Business & Loans

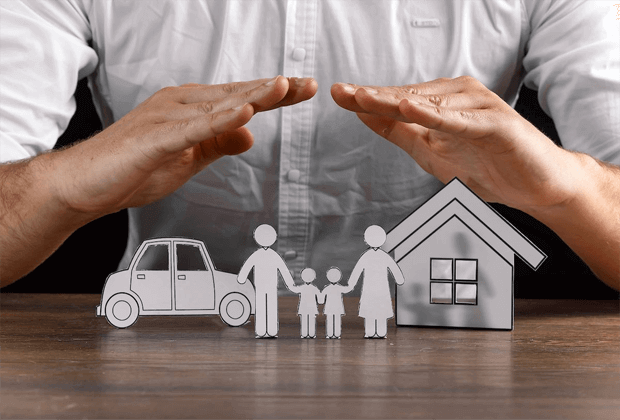

How To Easily Get Loan From Your Insurance Company

How To Easily Get Loan From Your Insurance Company

You might be wondering if it’s even possible to get a loan from your Insurance Company, the answer is yes, it is possible and in this article, we will be walking you through the procedures on how to obtain a loan from your Insurance company, so keep reading.

Many consumers are unaware that they may be able to borrow money from their insurance provider. You now know if you are one of those “many”. You might be able to borrow money from your insurance provider. How is that even possible, you ask? You don’t need to worry. You are on the right informational page. We will specifically cover how to obtain a loan from your insurance company in this article. We will also go over some other crucial ideas related to the topic.

You may also want to read 12 Top Instant Loan Apps Without BVN In Nigeria

How Can I Get a Loan From my Insurance Company?

The point is that, as we have mentioned, you might be able to borrow money from your insurance company. However, only having life insurance coverage makes this possible. We think there are some things you should be aware of even if borrowing against your life insurance might be a convenient way to secure a loan. It’s crucial to remember that you can only borrow against a permanent or whole life insurance policy. Additionally, whether you pay or not, your life insurance provider will add interest at the end of the month.

How Does a Life Insurance Loan Work?

This kind of financing is entirely distinct from a typical bank loan. This is so that it won’t have an impact on your credit. Additionally, since credit checks are not required, you do not have to go through the approval stage.

In actuality, you are not required to disclose to anyone how you intend to utilize your policy when you borrow against it. You are entirely free to choose what you want to buy with it. Aside from all of these advantages, one more is that tax regulatory authorities do not recognize this form of a loan. It is therefore tax-free. You should be aware that you will still be required to repay the loan in full, plus any accumulated interest. Although you do not have to pay on a monthly basis, the interest rate is far cheaper than traditional bank loans.

You may also want to read How To Easily Get a Personal Loan in 8 Steps

How Do I Repay My Loan?

The interest rate is low, and the repayment terms are flexible, as we have mentioned. In other words, the monthly repayment is not required of you. You must still repay the money you borrowed, though, so it doesn’t matter what else happens. You must make sure that you repay the debt in a timely manner in addition to paying it back. If you fail to do so, interest is charged to your debt and it continues to accrue whether you make monthly payments or not. You do not want to be in this circumstance. This is due to the impending likelihood of going over the policy cash value, which will result in the expiration of your policy value.

In Nigeria, insurance providers make sure that their customers have a variety of repayment options. This is done to make sure the loan is paid back in full and to avoid lapses. However, if the insured passes away, the insurance provider will tally up the loan’s principal and interest. Then, they will subtract it from the death benefit that the deceased’s intended recipients are supposed to receive.

Conclusion

Life insurance policy is a great way to get a loan from your insurance company, but it is important to repay when due. This is to avoid reducing your death benefit or even paying more out of your own pocket. If you would like to know more about this, you can contact your insurance company for more details.

Source: Flippstack

FG Presidential Conditional Grant Scheme Portal 2024 | Apply Now

Top 10 Easiest Countries To Migrate From Nigeria 2024

Nigeria Custom Service (NCS) Latest Recruitment 2024 – Application Portal

NDIC Latest Recruitment Application Portal 2024/2025 | www.ndic.gov.ng

FG Launches OTNI Job Creation Initiative To Provide 2,000 New Job Opportunities

EPL Game Week 30 Full Fixtures And Predictions 2023/2024

EPL Game Week 24 Full Fixtures And Predictions 2023/2024

NAF DSSC 32 2024 Latest Recruitment – Apply Now

-

Tips2 years ago

Tips2 years agoShiloh 2022 Programme Schedule – Theme, Date And Time For Winners Shiloh 2022

-

Business & Loans2 years ago

Dollar To Naira Today Black Market Rate 1st December 2022

-

Business & Loans2 years ago

SASSA Reveals Grant Payment Dates For December 2022

-

Jobs & Scholarship2 years ago

Latest Update On 2023 NPC Ad hoc Staff Recruitment Screening

-

Business & Loans2 years ago

Business & Loans2 years agoNpower Latest News On August Stipend For Today Friday 2nd December 2022

-

Business & Loans2 years ago

Dollar To Naira Today Black Market Rate 2nd December 2022

-

Business & Loans2 years ago

Business & Loans2 years agoNpower N-Tech Training: Npower Praises Female Trainees

-

Jobs & Scholarship2 years ago

Latest Update On Halogen Cyber Security Competition 2023

You must be logged in to post a comment Login